DISTRESSED VERSUS OBSESSED?

Knowing when the time is right takes FOCUS and EXPERIENCE

UNCERTAINTY? WITH GOVERNMENT FUNDING AND SUBSIDIES NO LONGER AVAILABLE, IT'S TIME FOR INDUSTRY PROFESSIONALS TO REFLECT ON WHAT THAT FUTURE SHOULD LOOK LIKE.

-

TIME TO RETHINK:

Do we really need so many customers? -

TIME TO REBUILD:

What are our real strengths and how do we optimize them? -

TIME TO RESTRUCTURE:

Are our resources, talent and management all they need to be?

Over the last 2-3 months, I have had conversations with some very qualified Agency Buyers, looking to take full advantage of the recessionary fears that appear to have cowed our industry into a state of somnolent caution as we look ahead to what 2023 might bring. The message being:

“Find me overwhelmed & distressed companies

that can be folded in without risk”

I fully understand the THRILL and operational upside of closing a “Killer Deal” and clearly recognise that the gradual reduction and ultimate removal of governmental support funding has left many smaller or younger organisations facing the new and often frightening reality of Vulnerability.

However, Experience has taught me that truly successful deal-making is more often about establishing real FIT and identifying Shared Ambitions and not simply the Strong gobbling up the Weak!!

This premise is particularly true for the strong, entrepreneurially led INDEPENDENTS, who have for the most part, met the pandemic crisis ‘head-on’ with well-structured cut-backs and total support for the real talent that has driven the businesses over time. For them the notion of distressed fold-ins makes much less sense versus filling operational or service gaps via acquisitions or merger partnerships with equally “OBSESSED” and Impassioned Sector Specialists or Regional Partners.

The immediate UNCERTAINTY facing serious Industry Professionals in these Recessionary Times dictates the Critical need to honestly appraise their business priorities and to establish their personal STRATEGIC PATHWAY whether to Downsize - Consolidate – Sell – structure an eventual EXIT– Raise Investment - find a Merger Partner or grow via Acquisition.

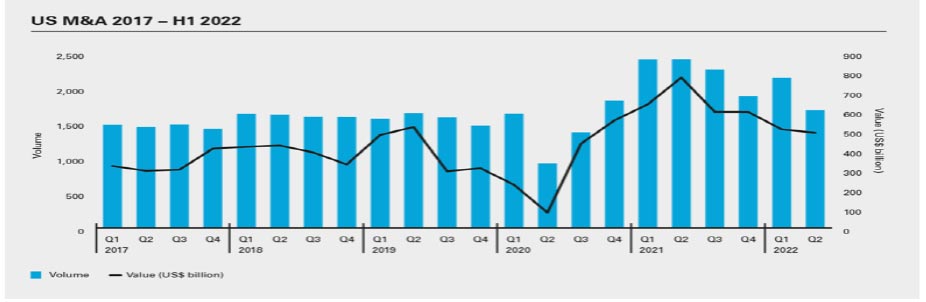

From a broader Industry perspective 2021 was a banner year for deal-making at scale. Companies like Accenture closed over 40 deals and ambitious valuation multiples (x8 to x12) abounded, as Private Equity groups dipped into their latent “Dry Powder”.

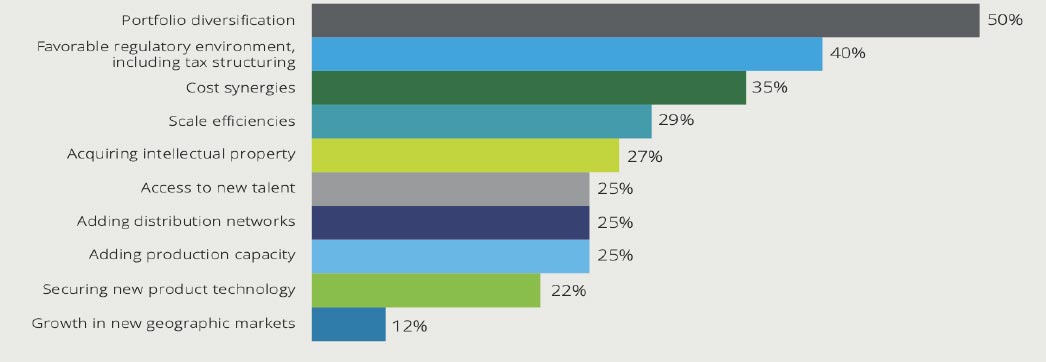

Strategic Deal Drivers - 2021

The 2022 numbers match healthy, pre-pandemic levels and are especially notable in what has lately been a time of great UNCERTAINTY.

Geopolitical instability, spiking inflation, supply chain issues, skittish capital markets, regulatory changes—all these factors, and more, are fueling that uncertainty.

The technology, media, and telecommunications sector (TMT) has outperformed other industries— accounting for 30 percent of total deal value.

From a Canadian Independent point of view, it’s great to see the sustained profitable growth of the EVOLVE Agency Group, proving that the strategic “Merger of Equals” that we envisioned, has brought continued commitment to Growth,new industry News and real, positive Momentum.

Similarly, the courageous expansion of No Fixed Address into the US and the West Coast continues to disrupt and make Mischief. Equally the successful mid-pandemic launch of Broken Heart Love Affair and the recent Expansion plans announced by Zulu Alpha Kilo emphasize the fact that entrepreneurial management and passionate and committed retained talent delivers abundantly. Meanwhile Quebec’s “dark horse” LG2 continues to flourish – already Canada’s largest “Indie”- ready to grow nationally?

As far as the Multinationals are concerned, the sustained commitment to structured talent retention and acquisition are clearly ‘front of mind’. Multi-brand consolidations are slowly paying dividends however, and many took advantage of the post pandemic rebound to make deals count.

See the deals made by some of the major Industry players:

- Consultants still leading the way with 92 deals

- Multinational Agencies also picked up the pace – 79 deals adding Digital and Performance Media capabilities.

- Larger Independents snagged 23 Deals

- Perhaps the most impressive moves were made by STAGWELL, who continue to rise from the residue of MDC.

- They have steadily built a large scale, multidimensional, international organisation focused on PERFORMANCE MARKETING – claiming to be 57% digitally-driven by end 2022.

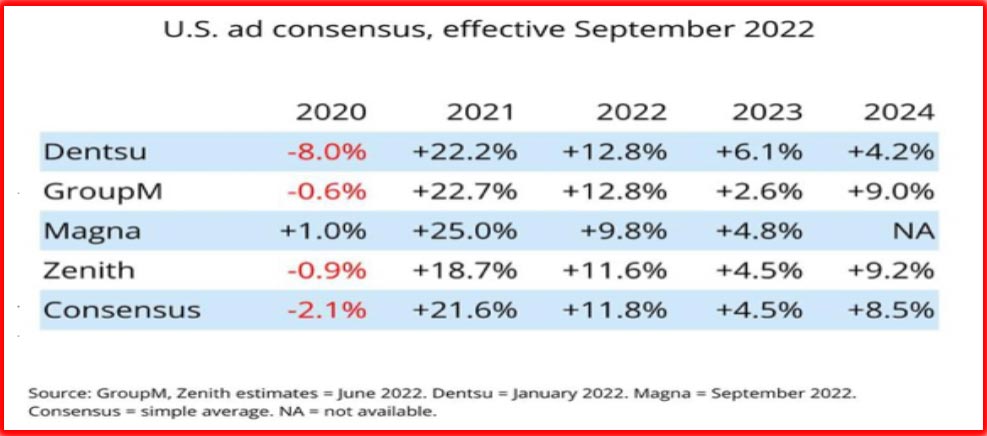

As we look ahead to 2023, our industry can take some comfort in the following Forecast for Advertising Expenditures, as published by Media Post in September 2022:

My personal belief is that Q1 2023 is the time for Agency Owners across the Americas to focus on the realities of an over-saturated agency world, without the government subsidies.

It’s time for honest reflection and to begin working with a qualified ‘industry-focused’ M&A Advisor and together map out a STRATEGIC PATHWAY to the future.

Whether the decision is SELL now, prepare an eventual EXIT strategy, find a MERGER PARTNER, or GROW by acquiring new, scalable service capabilities or expanded geographic coverage, it is essential to build a definitive and strategically relevant, Customised Plan.

In my past life as an Agency Owner, I always felt that leadership of an SME business can be lonely in the extreme. It is rarely a short-term affair and more often than not, it requires a deeply personal and financial commitment to a Life Journey.

If any Owners and Professional Managers are seriously thinking about their future and envisioning M & A Success as a key part of that future, I look forward to hearing from you and having an initial candid conversation — NOW IS THE TIME.

Kevin Astle is the Founder and Managing Partner of MultiVisory International. Having worked on both sides of the Atlantic and on both sides of the Client/Agency desk across North America, he brings an international perspective and deep, multi-sector knowledge and network to his Clients.