As the Old Guard consolidates in the Advertising and Marketing Services Sectors, can the Digital Upstarts and Integrated Independents drive the Industry’s Momentum Rebuild?

COVID 19 impacted many of the World’s service industries with significant revenue and job losses, emptied premium urban office spaces and taught staffers how to work productively from home, all while leaving behind a pervasive sense of UNCERTAINTY. Current data tells us that more than 3.5million Small to medium business enterprises in North America closed their doors on a permanent basis, while others relied extensively on governmental subsidies to keep them afloat. Few business sectors felt that Pandemic impact as severely as the Advertising and Marketing Services industry, where Clients held their aggregated breath for at least 90 days, (March through June) cancelling or postponing all marketing expenditures until they could take a considered view of the changing business landscape.

As the industry looks to 2021 with ‘reserved’ optimism as the promise of curative vaccines enhanced by the positive signs of gradual spending resurgence in the last 2 quarters of 2020, have delivered new hope for the future. That future may however be within a very different and rapidly evolving industry structure and agency profitability profile.

In recent times we have seen the emergence of the world’s leading Consultancy groups and Private Equity driven companies as the major growth engines for the industry. Only Dentsu Aegis Network of the long- established Multinational Agency groups have been actively pursuing acquisitive growth, while their industry peers have refocused on the consolidation of their diverse, ‘branded’ agency assets. That trend has now even overtaken Dentsu’s ambitions as they announced in November 2020 that they were working actively to consolidate 160 of their current agency brands into 6 focused global service agencies.

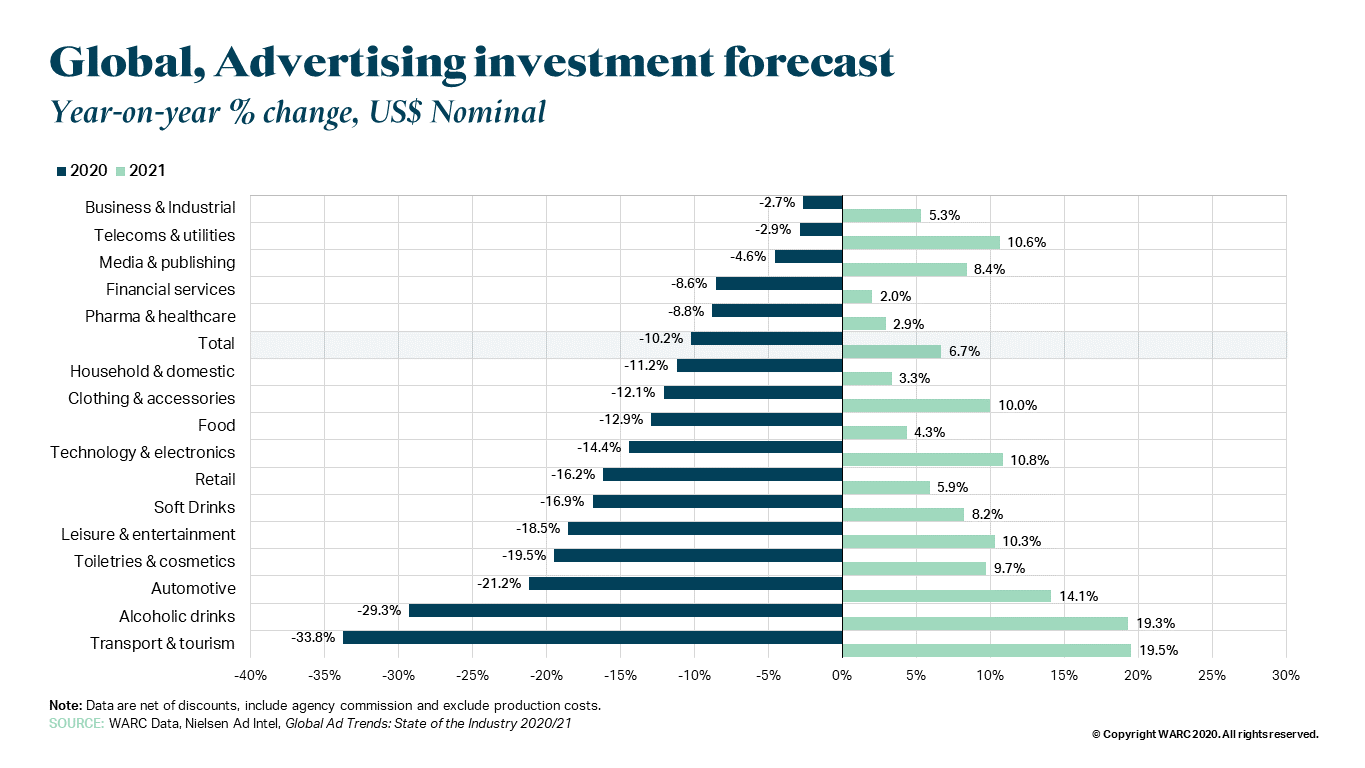

In the early weeks of 2021, Media Daily News published a consolidated and ‘dour’ view of the updated Global 2020 Ad Spend and 2021 Spending Forecasts from 4 of the leading global Multinational groups as follows:

As the Consensus line clearly demonstrates, we are unlikely to see any massive rebound in 2021 from the COVID driven cumulative losses incurred in 2020 – rather a question of stabilizing things in the hope of renewed robustness in 2022.

Looking beyond annual industry totals, we can also see that key component market sectors as reported by WARC, are in fact anticipating very different results:

In mid-January, Forrester Research also detailed their data-driven predictions for 2021, raising some interesting strategic dilemmas and interesting opportunities and urging brands to focus on becoming “customer obsessed” and to nurture “brand devotees”.

- 20% of Companies will not survive 2021

- Total Marketing Spend in N. America to decrease by 39% vs 2019 spending levels

- Digital Media, Social Advertising and Email Marketing to drive 60% of total Marketing $ by 2022

- Q4 2020 Recovery Levels hard to sustain, as pent-up Consumer Demand only kicks-in mid 2021

- Consumer Behaviour changes, with 50% staying away from crowds, 45% staying home more often and growing E-Commerce gains from consumer reticence (43%) to visit stores

- Digital Innovation accelerated "3years in 1" in 2020

- Decluttering of the Workforce and flattening out of Org structures has led to greater 'hands-on' CEO involvement and faster decision making

- Remote Working will increase by over 300% versus pre-Pandemic levels

- Employee Stress in W-F-H environment (31%) will become a key retention factor for Employers

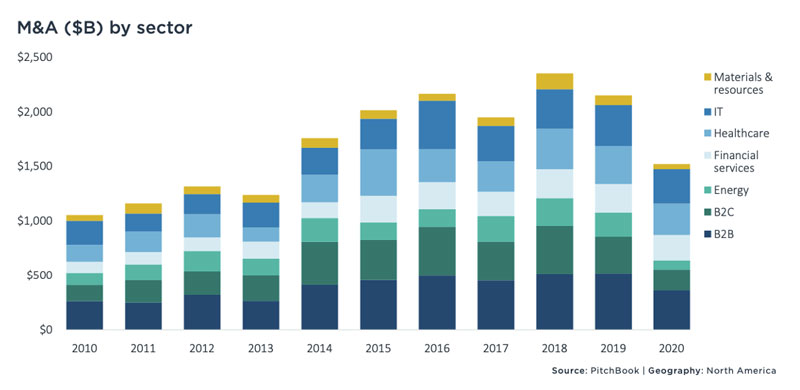

Pitchbook’s 2020 report on M&A activity in North America adds a different dimension to the overall picture with deal counts at 12,265 deals closed down by only 5.2% v.y.a, buoyed by strong healthcare and technology sectors. However, deal making values fell significantly by 21.5% versus 2019 levels.

On the positive side the smaller sized business deal counts have largely held their own and we have seen minimal evidence of aggressive ‘cut-throat’ deal making, whereby the bigger fish are swallowing up the minnows.

WHAT THEN ARE THE LOGICAL STRATEGIC OPPORTUNITIES OUT THERE FOR M&A LED ACTIVITY? PERHAPS IT’S A CASE OF “WHO DARES, WINS”.

Organizationally we’re definitely seeing on-going consolidation within the Multinational agency sectors and a significant slow-down in acquisition spending by the big Consulting groups, so perhaps it is time for the Independents to get aggressive and take back some measure of control. Using structured Merger and Acquisition strategies can help achieve sustainable business stability and increased service breadth relevance.

Seeking out Partners with shared ambitions and ‘real’ operational and talent synergies can definitely help optimize resource utilization and accelerate profitable growth.

There is a real opportunity for growing Digital agencies to “take the lead” and acquire established traditional agencies – breathing new life and re-energising creative passions. Equally, established Integrated Independents can look to merge in exciting, digitally driven Partners with a view to expanding strategic planning horizons and pulsing new blood across their agencies.

There is little doubt, that these pandemic times will change the agency landscape significantly. There are still way too many agencies out there and Clients will undoubtedly demand more accountability and partnership commitment from their agencies. Acting now to plan for future growth service-wise and/or geographically can help ensure sustainable profitability into 2022 and beyond as our world is gradually rebuilt.

When it comes to making major business decisions on whether to buy, sell or find a merger partner, my experience over the last 30years, has clearly evidenced that much as entrepreneurs want to control and fix things themselves, in times of change they are often too deeply ensconced in the day-to-day management of their business to handle the task. Rather it makes sense to find a professional advisor who has “walked the walk” and can help them objectively establish a clear Strategic Pathway, while also steering them away from the many pitfalls that cause deals to fail.

WHAT IS THE ADVISOR’S ROLE?

My belief is that the key is to immerse his or herself into the dynamics of a business and use this immersion to surface real strategic clarity. This ensures that the business owner makes informed and pragmatic choices about Growth, Consolidation and even Exit. Once that pathway is well defined, the Advisor’s mandate must be to establish final deal positioning, the targeting of potential Partners, qualifying interested parties, then negotiating the basic deal and facilitating due diligence and deal closure with accountants and lawyers. Finally add to the process an open-minded perspective and a focused desire to create a WIN-WIN outcome.

WHAT ARE THE KEYS TO MAKING A SUCCESSFUL DEAL?

Experience shows it is not simply Revenue gain or Cost savings, but rather strategic and cultural “FIT” at a management and operational level. Interestingly a recent quote by Seth Godin described the industry’s fixation with cost saving as the “race to the bottom”.

In reality, potential Deal Makers must look for an amalgam of inherent benefits to any deal, including operational efficiencies, complimentary service access, shared corporate ambitions and symbiotic cultural values.

Kevin Astle is the Founder and Managing Partner of MultiVisory International. Having worked on both sides of the Atlantic and on both sides of the Client/Agency desk across North America, he brings an international perspective and deep, multi-sector knowledge and network to his Clients.